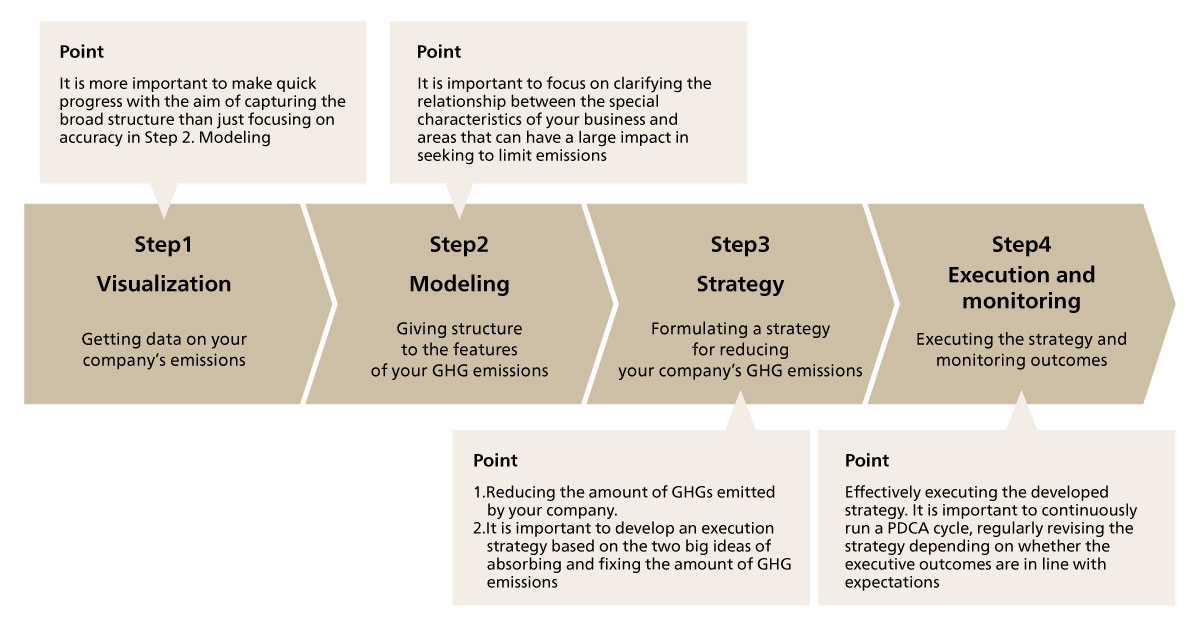

Decarbonization remains an important management theme, and many companies have already taken steps by collecting and publishing their emissions data as part of their sustainability activities. However, as far as I know, most companies do not have a system yet, and the necessary data is compiled manually from each department by the sustainability promotion department or the corporate planning department and published once a year. In addition, "1. Visualization" and "2. Modeling" have been implemented to a certain extent, but "3. Strategy" has only limited implementation and "4. Execution and Monitoring," especially the "monitoring" part, is just compiling numbers. There are few cases in which the complete PDCA cycle is used to ensure the company's strategic advantage.

Decarbonization will increasingly become a significant priority on the management agenda for companies in the future, and it will become necessary to incorporate sustainable decarbonization activities into corporate strategies, rather than simply making it an annual activity. The business infrastructure that supports these activities will change. In this chapter, we will consider the future vision of business infrastructure (systems) for achieving decarbonized management.

First we will define the business infrastructure. One is the ERP system that manages people, goods, and money (accounting, purchasing, sales, etc. , which are utilized in any corporate activity), and the other is the business system that reinforces competitive advantages in those activities. In which category should the infrastructure system for achieving decarbonization be positioned? From the perspective of "1. Visualization" and understanding and monitoring the impact on management (costs, etc.), it would be better to have that function in or in conjunction with the ERP system. From the perspective of Execution and Monitoring, it would be better to place that function in the business system.

The reason is that ERP systems contain data related to corporate activities (people, goods, and money etc.) and have a high affinity with linking GHG emissions emitted as a result of corporate activities to existing information (for example, linking it to accounting information to capture the correlation with cost impact). Entering sustainability information into the enterprise information system (entering invoices etc.) will also be useful for analyzing the overall correlation with the actual data. If business activities can be modeled, then there is a high possibility that GHG emissions and the effects of reductions can be seen in real time. However, business-related systems are intended to ensure the competitive advantage of a business, and incorporating mechanisms for executing GHG reduction strategies would be optimal for ensuring a competitive advantage. Treating decarbonization as a management agenda and running a PDCA cycle to maintain awareness of the overall process will be an important addition to the company's business infrastructure, and it will be important to assign functions in a balanced manner according to the properties of the system, etc.

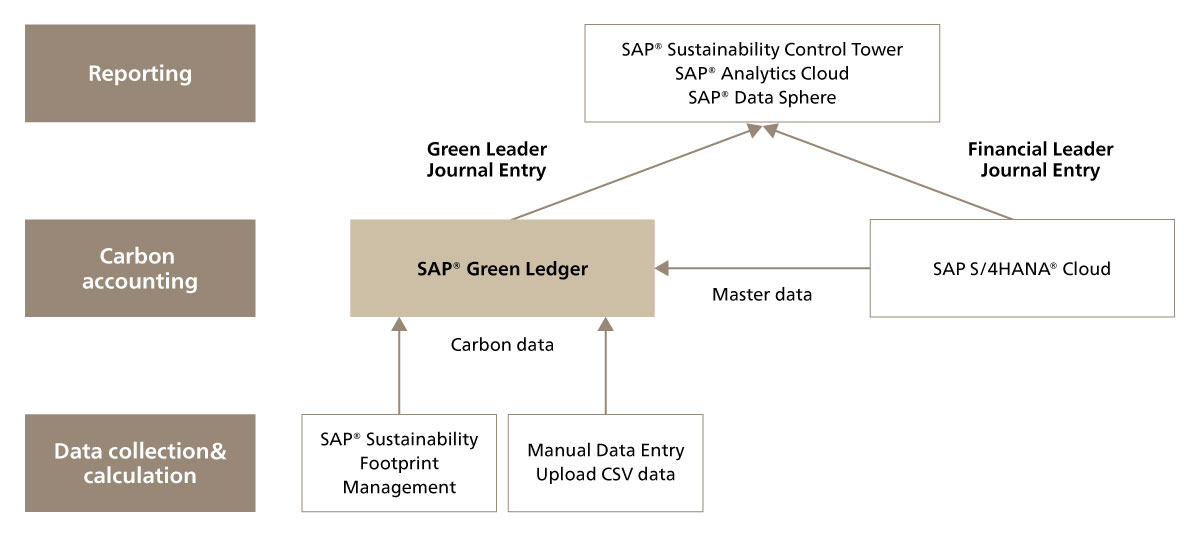

Many system vendors have recognized this situation and are attempting to seize dominance in the next business infrastructure. However, most of these systems are specialized in "Visualization," and there are no systems that embody the idea of incorporating GHG data into an ERP system. In December 2024, SAP (a major business infrastructure company) released a new service called "SAP® Green Ledger"*1. The details will be described later, but the idea is to link and visualize ERP system information (accounting) to GHG emissions information (carbon) and make them visible for future deployment to achieve true decarbonized management. The fact that SAP, who holds the market leader in packaged software for business infrastructure for large enterprises, has begun such an initiative is an indicator that the world is moving towards the future envisioned by this Insight.

ABeam Consulting has begun offering support for building digital platforms that integrate the management of financial and non-financial data for collection and disclosures of sustainability data, in coordination with ERP systems (SAP, etc.). In January 2025, we entered a strategic business alliance with boost Sustainability Cloud, an integrated SX platform that automates collection and aggregation of sustainability data and allows real-time monitoring based on international standards. The platform has a strong track record and is used by about 2,000 companies in over 80 countries (186,000 locations or more as of November 2024). We look forward to continuing to offer clients multifaceted implementation support, including the integrated construction of systems that match the unique characteristics of their businesses.

Reference: Press release, “ABeam Consulting in Strategic Business Alliance with booost technologies” (Japanese)

Many companies are exploring ways to achieve decarbonized management. Those that work towards decarbonization in the medium to long term, over the next decade will maintain their competitive advantage. It will be necessary for them to prepare swiftly, consistently, and sustainably through "1. Visualization," "2. Modeling," "3. Strategy," and "4. Execution and Monitoring." Business infrastructure updates do not come frequently, so it will be a good idea to take advantage of the timing of system updates to prepare the entire business infrastructure for decarbonized management-ready features and consider incorporating the functions of SAP® Green Ledger or booost Sustainability Cloud.

One option may be to utilize a consulting firm such as ours, which provides comprehensive and integrated support to renew business infrastructure systems and efforts toward GX. We encourage companies considering constructing a business infrastructure for decarbonization to contact us.